Compounding interest – is this the greatest mathematical discovery in human history? I have always been fascinated by the concept and power of compounding. In financial terms, compounding refers to the process of earning the returns on principal (the original amount you invested) plus the return that was earned earlier.

Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it. – Albert Einstein

It is a simple principle and we all understand it. But to practice it is another thing altogether. Maybe it’s because you need to be consistent and give it time before you can see it works its wonders. Nevertheless, the concept of compounding interest is very powerful. It is the essence of wealth creation towards your path to financial freedom.

I have learned about this concept more than twenty years ago but I think I have not really harness its magical powers consistently. Otherwise I believe I would be in an even better financial position today.

The good news is, it is always never too late to start, so I decided to write about compounding interest as a form of reminder to myself to work with it always.

There are three components for the financial compounding concept to work:

- Capital (Seed money)

- Time (Period invested)

- Rate of Return (% per year)

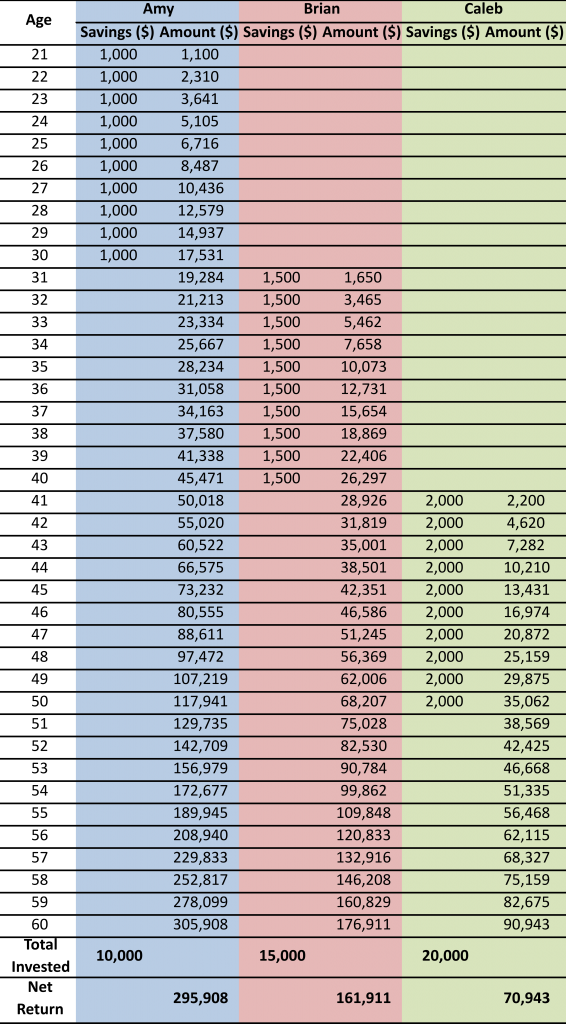

To illustrate how these three components of the power of compounding come into play, I like to use the example of three investors: Amy, Brian and Caleb.

Say Amy invests $1000 a year for a total of 10 years from age 21 to 30. After the age of 30 she stops investing. Brian on the other hand waited till his older thinking that he can invest more when he is ready to start investing. So from age 31 he started putting in $1500 a year for the next 10 years. Lastly, Caleb only woke up and realized that he needs to save at the age of 41. Trying to catch up, he puts in $2000 a year for 10 years, believing it is not too late to catch up.

For this example, let us assume that Amy, Brian and Caleb were all able to invest at a compounded return of 10%. The results of their investment when all three of them 40 years later, when they are ready to retired at age of 60, can be shown in the table below.

As you can see, the difference in net returns from our three investors is astounding!

Amy only invested a total of $10,000. Her return, minus of her investment amount is $295,908.

Brian invested a total of $15,000. For that his return minus his investment amount is $161,911.

I don’t have to tell you how miserable Caleb’s net return is even though he put in the most money.

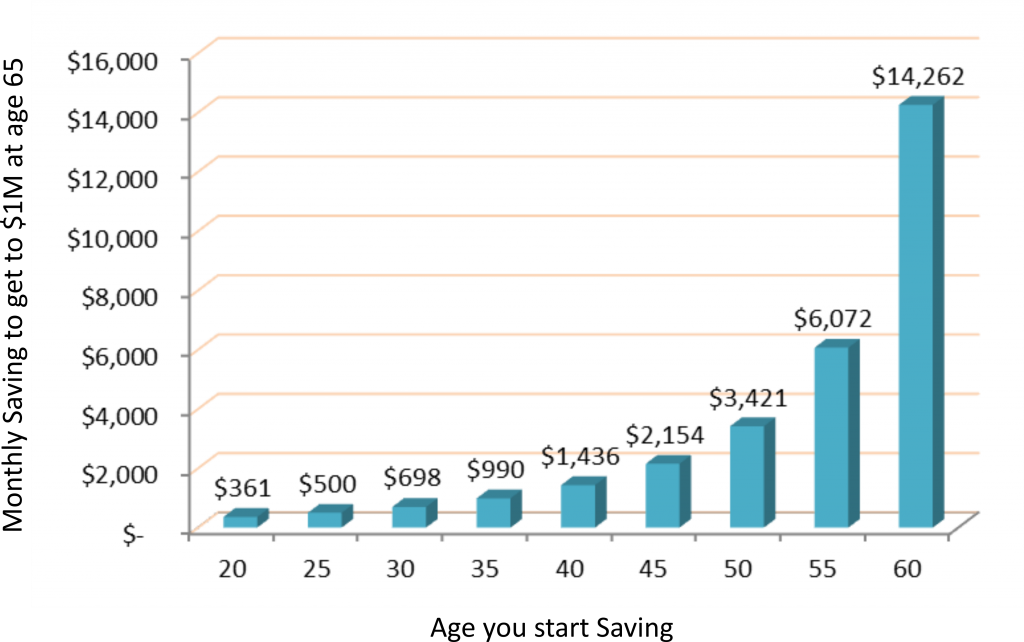

Let’s look at another illustration. How much money do you think you will need to save each month if you want to retire with one million at the age of 60? Let’s assume this time that you are able to obtain an annual return of 6% consistently each year.

As you can see, when it comes to savings, time is really your best friend. If you have started saving at 20, all you need to put aside is $361 a month. This translates to a total of $194,940 put in savings over the course of 45 years and compounding interest tops up the balance to give you a total of $1,000,000.

On the other hand if you only start at 55, you will need to save about $6,072 monthly just to end up with the same $1,000,000 at 65. The difference is you would have put in close to $730,000 in that 10 years just to enjoy that same million. Ouch!

From the two simple illustrations we can draw two very valuable insights:

1 – When you start investing is more important than how much you save

Amy started investing young. Even though the amount she saved each year is lesser than Brian and Caleb, she eventually emerged the winner with the most net return.

What this tells us is that we should not wait to have more before we start to save. We must start to save now, regardless the amount in order for us to have more later.

2 – You have the power and ability to benefit from the principle of compounding

The beauty of the compounding lines in the ability for us to control the above three components to our advantage. You can decide how much money you are going to invest and how long you are going to stay invested.

We cannot specifically control the rate of return on the investment; however we do have a choice in choosing from different investment vehicles that will offer different rates of return, depending on our risk appetite.

The workings of compounding interest is indeed powerful. No matter where you are financially today, put this principle to good use and you will surely reap the rewards in the years to come.

Now I wonder how the compound effect will work on running!